OAuth vs API Keys Explained: Differences, Security & Use Cases (2026)

Understanding OAuth vs API keys is essential for securing modern applications. APIs require authentication methods to verify users and systems, and choosing the right approach directly impacts security and scalability.

In India and globally, fintech, banking, and SaaS platforms rely on authentication systems like OAuth and API keys to protect sensitive data and enable secure communication.

What are API Keys

API keys are simple authentication tokens used to identify the calling application.

Key features:

- Easy to implement

- Static token-based authentication

- Used in headers or query parameters

- Suitable for basic use cases

What is OAuth

OAuth (Open Authorization) is an advanced authorization framework that allows secure access without sharing credentials.

Key features:

- Token-based authentication

- Delegated access

- Supports user consent

- Secure and scalable

https://oauth.net/2/

https://www.rfc-editor.org/rfc/rfc6749

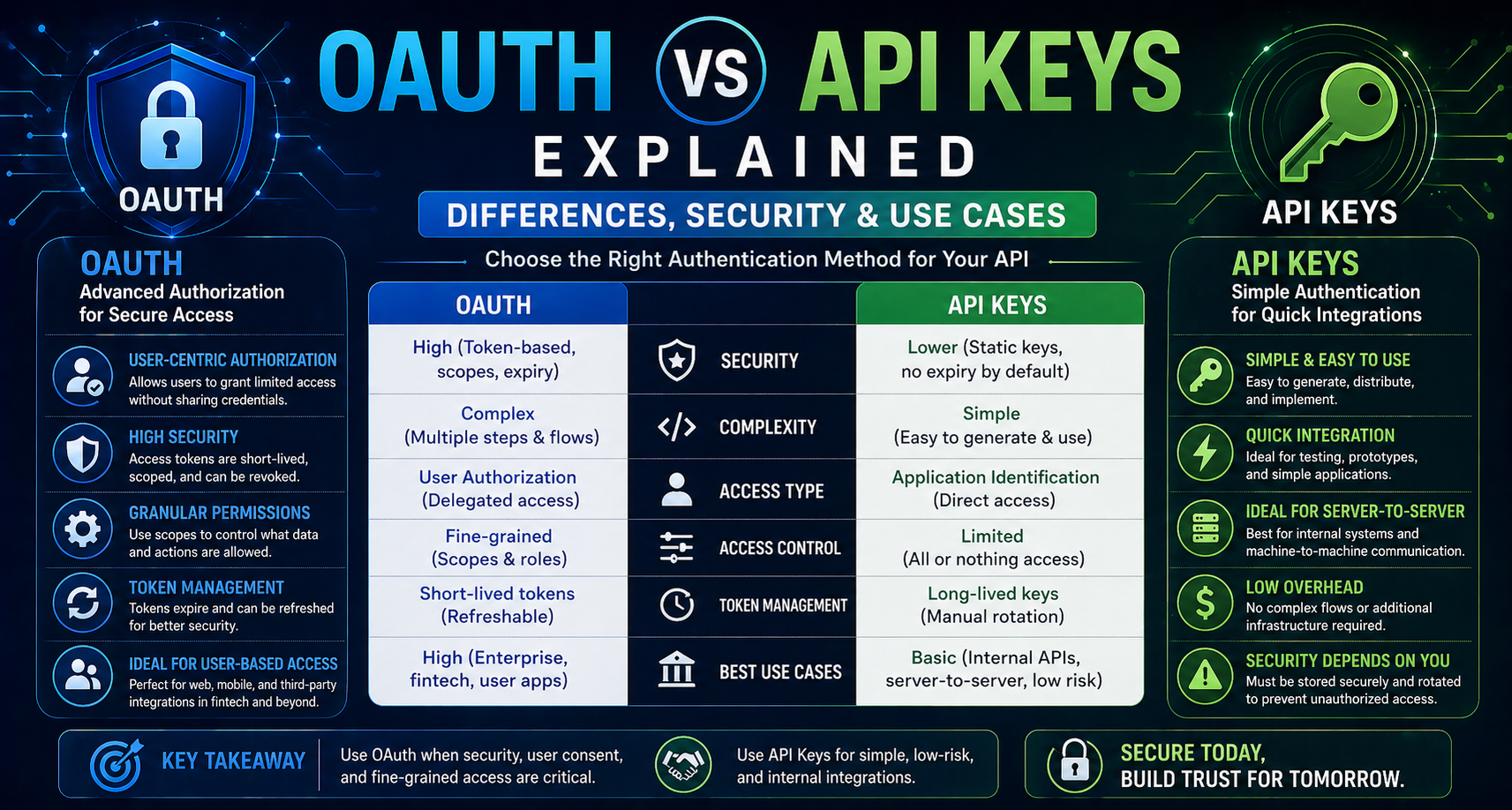

Key Differences: OAuth vs API Keys

Security

OAuth provides higher security with token expiration and scopes. API keys are less secure as they are static.

Complexity

API keys are simple to implement, while OAuth requires more setup and configuration.

Use Case

API keys are used for simple applications. OAuth is used for secure and complex systems.

Access Control

OAuth supports role-based and scoped access. API keys provide limited control.

Token Management

OAuth tokens expire and can be refreshed. API keys usually remain constant.

When to Use API Keys

API keys are suitable for:

- Internal APIs

- Low-risk applications

- Simple integrations

- Server-to-server communication

When to Use OAuth

OAuth is ideal for:

- Fintech applications

- Banking systems

- User-based authentication

- Third-party integrations

https://nxtbanking.com/dmt-api

https://nxtbanking.com/bbps-api

Advantages of API Keys

Simplicity

Easy to generate and use.

Quick Integration

Minimal setup required.

Lightweight

No complex authentication flow.

Disadvantages of API Keys

Low Security

Keys can be exposed if not handled properly.

No Expiration

Static keys increase risk.

Limited Access Control

No fine-grained permissions.

Advantages of OAuth

Strong Security

Token-based system with expiration and scopes.

Delegated Access

Users can grant limited access.

Better Control

Granular permissions and roles.

Industry Standard

Widely used in fintech and enterprise systems.

Disadvantages of OAuth

Complexity

Requires setup and understanding of flows.

Implementation Time

Takes longer to integrate.

OAuth Flow Explained

Basic OAuth flow:

- User logs in

- Application requests permission

- Authorization server validates user

- Access token is issued

- Application uses token to access API

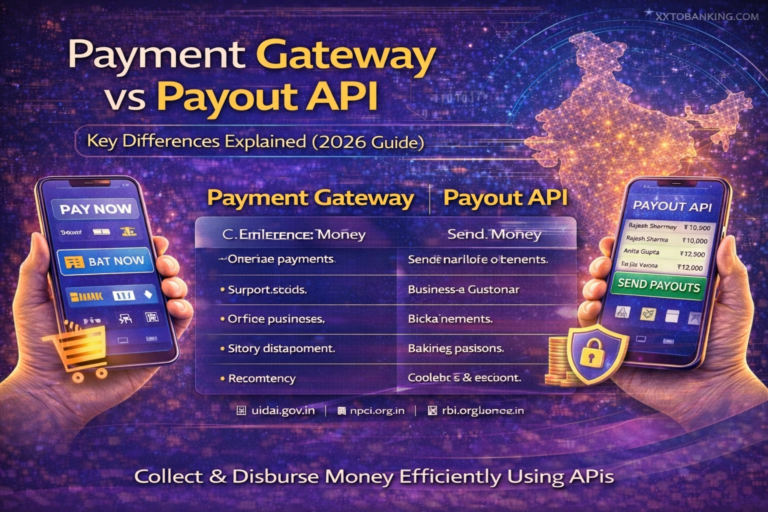

API Keys vs OAuth in Fintech

In fintech, security is critical. The choice between OAuth vs API keys depends on application requirements.

- API keys for internal systems

- OAuth for customer-facing platforms

https://www.rbi.org.in/

https://owasp.org/www-project-api-security/

Best Practices for Using API Keys

Restrict Usage

Limit API key usage by IP and domain.

Rotate Keys

Change keys regularly.

Store Securely

Do not expose keys in frontend code.

Best Practices for Using OAuth

Use HTTPS

Always use secure communication.

Implement Token Expiry

Use short-lived tokens.

Use Scopes

Limit access permissions.

Monitor Usage

Track token usage and revoke if needed.

Common Mistakes to Avoid

Exposing API Keys

Never store keys in public repositories.

Ignoring Token Expiry

Always manage token lifecycle.

Weak Authentication

Use strong validation methods.

Conclusion

The comparison of OAuth vs API keys highlights that both have their use cases. API keys are simple and useful for basic integrations, while OAuth provides advanced security and control.

For fintech and secure applications, OAuth is the preferred choice due to its robust authentication and authorization features.

https://nxtbanking.com/contact

About This Topic

The NxtBanking blog is India's authoritative technical resource for fintech API integration — covering Payout API, BBPS, AEPS, UPI, KYC, DMT, recharge APIs, and enterprise payment infrastructure. Every article is written by practitioners who have built and scaled payment systems processing millions of transactions, combining technical accuracy with real-world implementation guidance for developers, product teams, and fintech founders.

Quick Answers

What makes a good fintech API integration?

A well-built fintech API integration covers: proper OAuth 2.0 authentication, idempotency keys on every write request, webhook HMAC signature verification, exponential-backoff retry logic for transient errors, and a status-query fallback for ambiguous outcomes. NxtBanking's sandbox environment lets you test all these scenarios before production.

How do I handle failed transactions in a payment API?

Categorise failures: (1) Hard failures (invalid account, KYC mismatch) — do not retry; notify user. (2) Transient failures (timeout, 5xx) — retry with idempotency key and exponential back-off. (3) Ambiguous (no response) — call the transaction status endpoint before retrying to avoid duplicate processing.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

Key Terms

- API

- Application Programming Interface — a structured software interface that lets applications communicate with each other over the internet using defined endpoints, authentication, and data formats.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.