Fintech Business Models Explained: Types & Revenue Strategies (2026 Guide)

Understanding fintech business models explained is essential for anyone planning to enter the financial technology space. Fintech companies use innovative technology to deliver financial services efficiently, often disrupting traditional banking systems.

In India, fintech growth is driven by digital payments, API-based infrastructure, and increasing smartphone adoption. Choosing the right model is crucial for building a scalable and profitable fintech business.

https://nxtbanking.com/dmt-api

https://nxtbanking.com/bbps-api

What is a Fintech Business Model

A fintech business model defines how a company:

- delivers financial services

- generates revenue

- interacts with users

- scales operations

It determines the structure, pricing, and long-term sustainability of the business.

Why Understanding Fintech Business Models is Important

Better Strategy

Helps define clear goals and operations.

Revenue Planning

Identifies how the business will earn money.

Scalability

Ensures the model supports growth.

Investor Attraction

Clear models attract funding and partnerships.

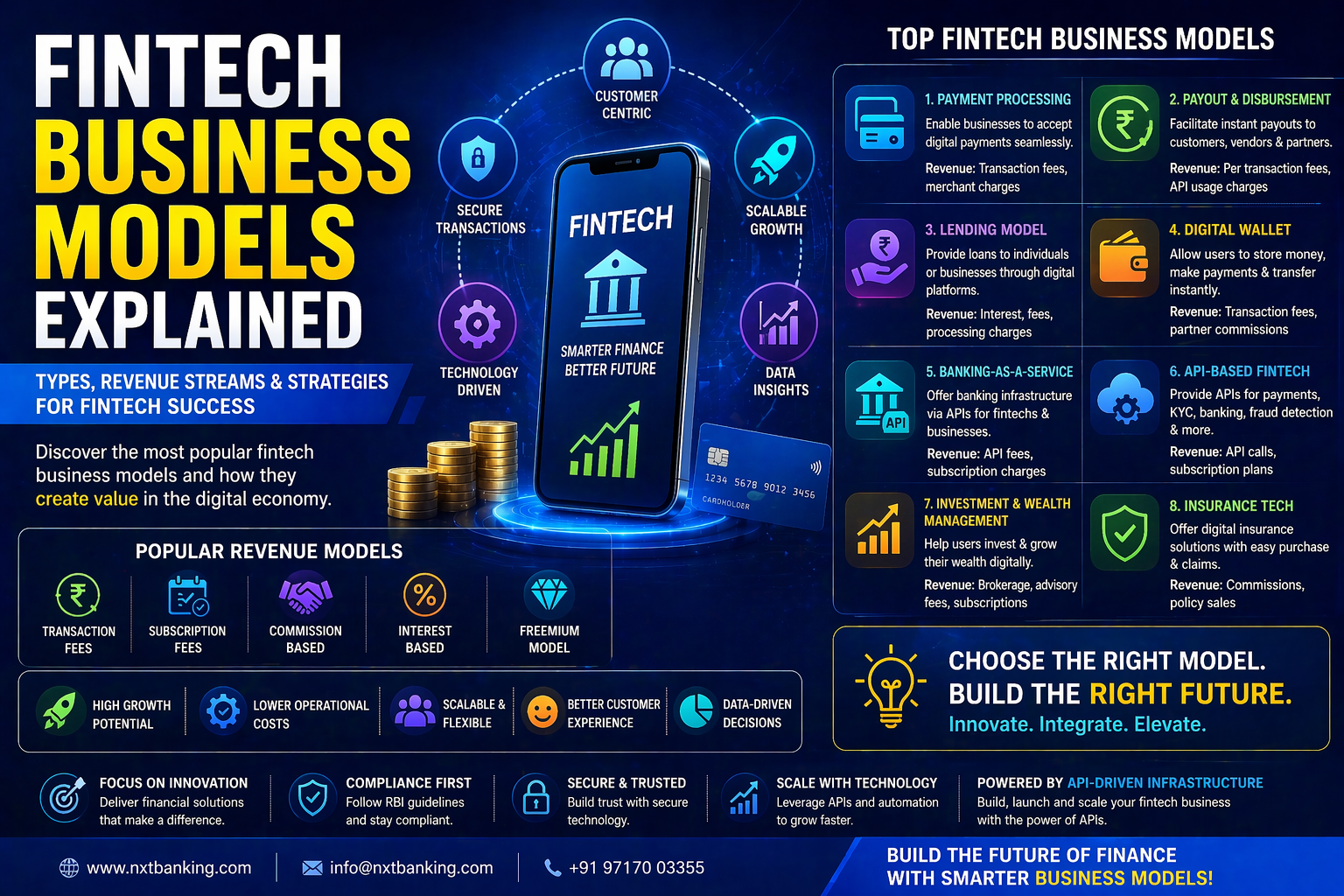

Fintech Business Models Explained

Payment Processing Model

Companies provide services to accept payments online.

Examples:

- payment gateways

- checkout systems

- UPI integrations

Revenue sources:

- transaction fees

- merchant charges

Payout and Disbursement Model

Businesses provide APIs to send money to users.

Use cases:

- salary payments

- vendor payouts

- refunds

Revenue sources:

- per-transaction fee

- API usage charges

https://nxtbanking.com/payout-api-how-it-works/

Lending Model

Platforms provide loans to individuals or businesses.

Types:

- personal loans

- business loans

- BNPL

Revenue sources:

- interest

- processing fees

Digital Wallet Model

Users store money digitally and make transactions.

Features:

- wallet balance

- peer-to-peer transfers

- bill payments

Revenue sources:

- transaction fees

- partner commissions

Banking-as-a-Service (BaaS) Model

Provides banking infrastructure via APIs.

Startups can build financial products without becoming banks.

Revenue sources:

- API usage fees

- subscription charges

API-Based Fintech Model

Companies provide APIs for:

- payments

- KYC

- banking

- fraud detection

Revenue sources:

- API calls

- subscription plans

Investment and Wealth Management Model

Platforms help users invest in:

- stocks

- mutual funds

- crypto

Revenue sources:

- brokerage fees

- subscription

- advisory fees

Insurance Tech Model

Provides digital insurance services.

Revenue sources:

- commissions

- policy sales

Popular Fintech Revenue Models

Transaction-Based Revenue

Earn per transaction processed.

Subscription Model

Charge monthly or yearly fees.

Commission-Based Revenue

Earn a percentage from partners.

Freemium Model

Basic services are free, premium features are paid.

Interest-Based Revenue

Earn through lending services.

Role of APIs in Fintech Business Models

APIs are central to modern fintech.

They enable:

- automation

- scalability

- faster development

- integration with banks

Systems are often connected through networks managed by National Payments Corporation of India.

https://www.npci.org.in/

https://www.rbi.org.in/

Choosing the Right Fintech Business Model

Consider:

- target audience

- regulatory requirements

- technology capabilities

- revenue potential

- scalability

Selecting the right model is critical for long-term success.

Benefits of Fintech Business Models

- scalable operations

- digital-first approach

- high growth potential

- automation

- improved user experience

Challenges

Regulatory Compliance

Strict financial regulations must be followed.

Security Risks

Handling sensitive financial data requires protection.

Competition

Highly competitive market.

Technology Complexity

Requires strong development capabilities.

Future of Fintech Business Models

The future of fintech business models explained includes:

- embedded finance

- API-first platforms

- AI-driven financial services

- real-time payments

- decentralized finance

India will continue to lead fintech innovation globally.

FAQs

What are fintech business models

They define how fintech companies provide services and earn revenue.

Which fintech model is best

It depends on your business goals and target market.

Are fintech businesses profitable

Yes, with the right model and execution.

Do fintech startups need APIs

Yes, APIs are essential for scalability and automation.

Conclusion

Understanding fintech business models explained helps entrepreneurs choose the right strategy for building successful fintech platforms. With multiple models available, businesses can select the one that aligns with their goals, resources, and market demand.

The key to success lies in combining the right business model with strong technology, compliance, and customer experience.

https://nxtbanking.com/dmt-api

About This Topic

The NxtBanking blog is India's authoritative technical resource for fintech API integration — covering Payout API, BBPS, AEPS, UPI, KYC, DMT, recharge APIs, and enterprise payment infrastructure. Every article is written by practitioners who have built and scaled payment systems processing millions of transactions, combining technical accuracy with real-world implementation guidance for developers, product teams, and fintech founders.

Quick Answers

What APIs does NxtBanking provide?

NxtBanking provides 18+ fintech APIs on a single platform: Payout (IMPS/NEFT/RTGS/UPI), BBPS Bill Payment, AEPS, UPI Collection & QR, KYC & Identity Verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), Mobile & DTH Recharge, Domestic Money Transfer, Micro-ATM, Pay-In/Escrow, and Travel (Bus, Hotel, Air, IRCTC).

How long does NxtBanking API integration take?

Sandbox access is available immediately after sign-up. For most APIs, a developer can complete sandbox integration in 2–5 business days. Production go-live, including KYC, compliance review, and bank account setup, takes 7–21 business days depending on the API type.

What support does NxtBanking provide during integration?

NxtBanking provides dedicated technical onboarding (email + video call), comprehensive API documentation with Postman collections and code samples, a sandbox with simulated error scenarios, and email/chat support for integration queries. Enterprise accounts get a dedicated technical account manager.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.