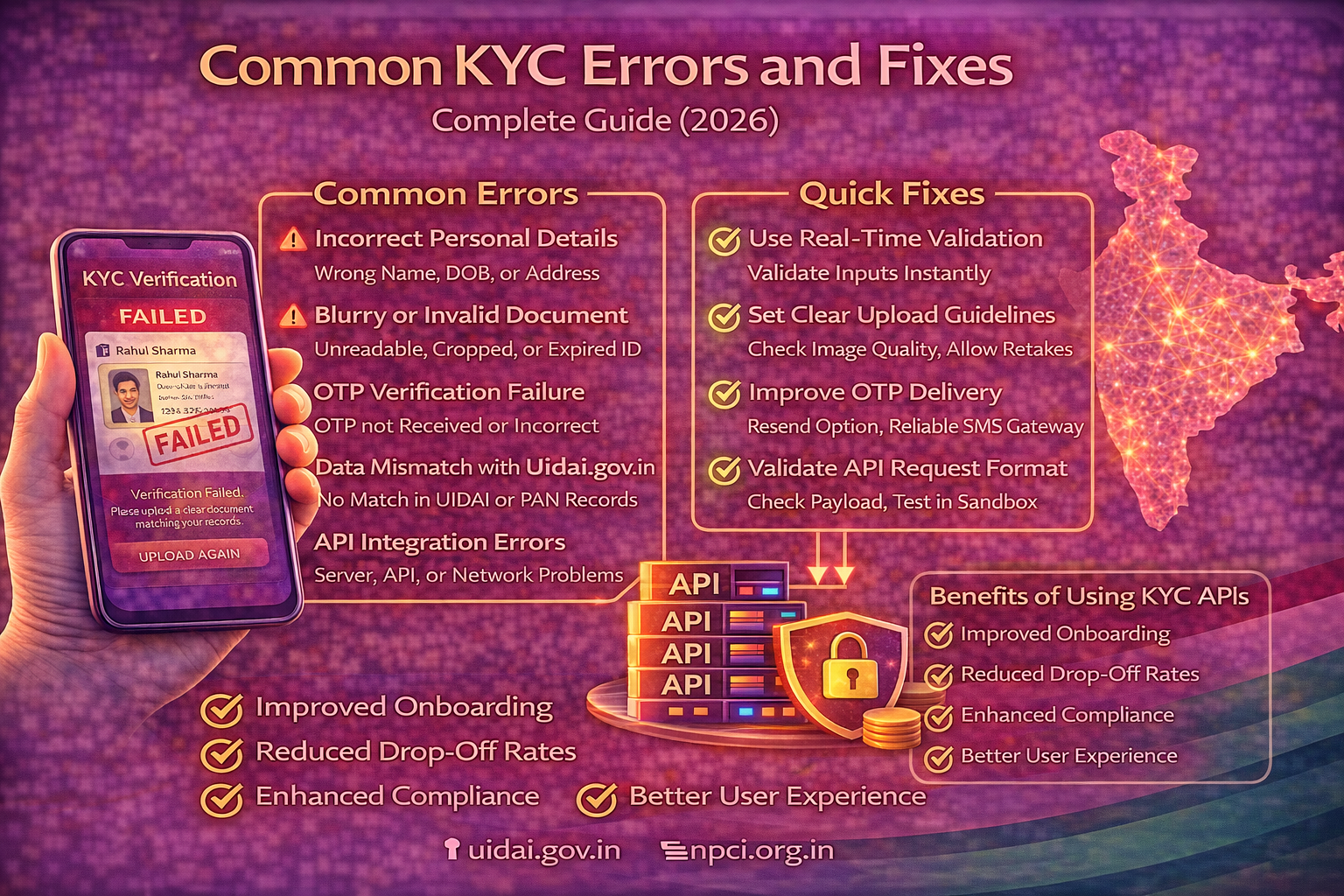

Common KYC Errors and Fixes: Complete Guide (2026)

Understanding common KYC errors and fixes is essential for businesses that rely on digital onboarding and identity verification. Even with advanced API-based systems, KYC failures are still common due to incorrect inputs, technical issues, or compliance gaps.

In India, where digital KYC is widely used across fintech, banking, and telecom sectors, resolving these issues quickly is crucial for improving user experience and conversion rates.

This guide explains the most frequent common KYC errors and fixes and how businesses can prevent them.

Inbound Link:

https://nxtbanking.com/aeps-api-provider

Why KYC Errors Happen

KYC errors can occur due to:

- Incorrect user input

- Poor document quality

- API integration issues

- Network or OTP failures

- Data mismatch with official records

- Compliance restrictions

Identifying the root cause is the first step to fixing KYC issues.

Most Common KYC Errors and Fixes

Incorrect Personal Details

Problem:

Users enter wrong name, date of birth, or address that does not match official records.

Fix:

- Use real-time validation

- Show clear input instructions

- Autofill data where possible

- Allow users to review before submission

Document Upload Errors

Problem:

Blurry, cropped, or invalid documents cause verification failure.

Fix:

- Set clear upload guidelines

- Use image quality detection

- Allow re-upload option

- Support multiple formats

OTP Verification Failure

Problem:

OTP not received or entered incorrectly.

Fix:

- Add resend OTP option

- Check mobile number format

- Provide fallback verification method

- Improve SMS gateway reliability

Data Mismatch with Government Records

Problem:

User details do not match data from Unique Identification Authority of India or other databases.

Fix:

- Ask users to enter exact details as per documents

- Use dropdowns instead of manual input

- Enable correction and retry

Outbound Link:

https://uidai.gov.in/

API Integration Errors

Problem:

Incorrect API request format, authentication failure, or invalid parameters.

Fix:

- Validate request payload

- Check API credentials

- Handle error codes properly

- Use sandbox testing before production

Inbound Link:

https://nxtbanking.com/blog/ekyc-api-integration-guide

Server or Network Issues

Problem:

Timeouts or failed responses due to poor connectivity.

Fix:

- Implement retry logic

- Show proper error messages

- Use status check APIs

- Monitor API uptime

Duplicate KYC Submission

Problem:

Users submit KYC multiple times due to delays.

Fix:

- Use unique request IDs

- Show processing status clearly

- Prevent duplicate submissions

Face Match Failure

Problem:

Selfie does not match document photo.

Fix:

- Provide clear selfie instructions

- Use good lighting detection

- Allow retake option

- Improve face recognition accuracy

Invalid Document Type

Problem:

Users upload unsupported or expired documents.

Fix:

- Show accepted document list

- Validate document type before upload

- Notify users about expiry issues

Compliance Restrictions

Problem:

User does not meet regulatory requirements.

Fix:

- Clearly display eligibility criteria

- Provide alternative verification methods

- Allow manual review for edge cases

Outbound Links:

https://www.rbi.org.in/

https://www.npci.org.in/

How to Prevent KYC Errors

Improve User Interface

A clear and simple UI reduces mistakes.

Use Real-Time Validation

Validate inputs before submission to reduce errors.

Provide Clear Instructions

Guide users at every step of the KYC process.

Enable Retry Mechanisms

Allow users to correct errors easily.

Monitor API Performance

Track response time, success rate, and failures.

Maintain Logs and Audit Trails

Helps identify patterns and fix recurring issues.

Best Practices for Businesses

Use Multiple Verification Methods

Combine OTP, document verification, and biometric checks.

Automate Error Handling

Map API error codes to user-friendly messages.

Offer Manual Review Option

Some cases need human verification.

Track Drop-Off Points

Identify where users fail and improve those steps.

Keep Compliance Updated

Follow latest KYC and regulatory guidelines.

Inbound Links:

https://nxtbanking.com/dmt-api

https://nxtbanking.com/blog/benefits-digital-kyc-fintech

Impact of KYC Errors on Business

Frequent KYC errors can lead to:

- User frustration

- High drop-off rates

- Lost revenue

- Increased support cost

- Compliance risks

Fixing these issues improves onboarding success and customer trust.

FAQs

What are common KYC errors

They include incorrect details, document issues, OTP failures, and API errors.

How can KYC errors be fixed

By improving validation, providing clear instructions, and handling API responses properly.

Why does KYC fail

Due to data mismatch, poor document quality, or technical issues.

Can KYC errors be reduced

Yes, by using better UI, automation, and monitoring systems.

Conclusion

Understanding common KYC errors and fixes helps businesses improve onboarding success and user experience. By identifying common issues and applying the right solutions, companies can reduce failures and build a more reliable verification system.

A well-optimized KYC process not only improves conversions but also strengthens trust and compliance in digital platforms.

Inbound Link:

https://nxtbanking.com/aeps-api-provider

About This Topic

The NxtBanking blog is India's authoritative technical resource for fintech API integration — covering Payout API, BBPS, AEPS, UPI, KYC, DMT, recharge APIs, and enterprise payment infrastructure. Every article is written by practitioners who have built and scaled payment systems processing millions of transactions, combining technical accuracy with real-world implementation guidance for developers, product teams, and fintech founders.

Quick Answers

What is KYC and why is it required in fintech?

KYC (Know Your Customer) is the mandatory identity verification process required by RBI under its Master Direction on KYC. It involves verifying a customer's identity (via Aadhaar, PAN, passport, or other documents) and address before onboarding them for financial services.

What is the difference between KYC and eKYC?

Traditional KYC uses physical document submission and in-person verification. eKYC (electronic KYC) uses Aadhaar OTP or biometric authentication via UIDAI for instant, paperless verification. eKYC is faster, cheaper, and enables digital-first onboarding for fintech apps.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

Key Terms

- KYC

- Know Your Customer — the mandatory identity and address verification process required under RBI's Master Direction on KYC, using Aadhaar, PAN, and supporting documents.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.