BBPS Agent Model: How to Become a BBPS Service Provider

Understanding the BBPS Agent Model

The BBPS (Bharat Bill Payment System) agent model is one of India’s most attractive fintech business opportunities. With over 20,000+ billers on the platform and crores of monthly transactions, BBPS agents play a vital role in extending digital bill payment services to every corner of the country, especially in semi-urban and rural areas where digital literacy is still growing.

What is a BBPS Agent?

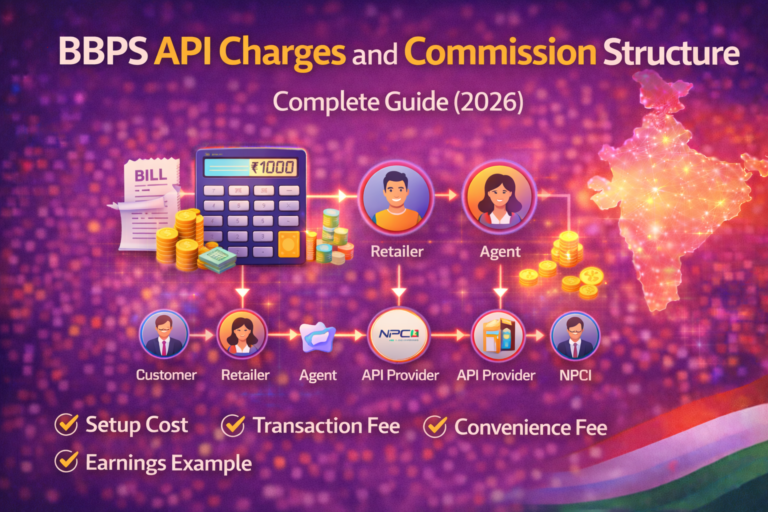

A BBPS Agent is an authorized entity or individual who collects bill payments from customers on behalf of billers. Agents operate through physical touchpoints (shops, kiosks, banking correspondents) or digital channels (apps, websites) and earn commission on every transaction.

The agent model operates under the Customer Operating Unit (COU) framework. A COU is licensed by NPCI and authorized by RBI. Agents work under a COU or Agent Institution (AI) that provides them with the technology platform and banking infrastructure.

BBPS Agent Ecosystem: Who’s Who

Agent Institutions (AIs)

Organizations that recruit and manage agents. AIs connect to BBPS through a COU and provide agents with the app/platform to process transactions. Banks, NBFCs, and authorized fintech companies can become AIs.

Individual Agents

Retail shop owners, mobile recharge outlets, banking correspondents, and CSC operators who interact directly with customers. They use an app or device provided by their AI.

Super Agents / Distributors

Mid-layer entities that recruit and manage a network of individual agents. They earn override commissions on their agent network’s transactions.

How to Become a BBPS Service Provider

Option 1: Partner with an Existing COU/AI

The fastest route. Companies like NxtBanking provide ready-to-use BBPS infrastructure. You sign up as an agent or distributor, get access to the platform, and start processing transactions.

Requirements:

- Valid business registration (GST, shop establishment)

- KYC documents (Aadhaar, PAN, address proof)

- Minimum working capital (varies by AI, typically ₹5,000 – ₹25,000)

- Smartphone or computer with internet

Option 2: Become an Agent Institution

For larger operations wanting to build their own agent network. This requires:

- Registration with NPCI as an Agent Institution

- Partnership with a licensed COU for BBPS connectivity

- Minimum net worth requirements (as specified by NPCI)

- Technology infrastructure for agent management

- Compliance framework (KYC, AML, dispute resolution)

Option 3: Become a COU (Full License)

The highest level. COUs connect directly to BBPS Central Unit. Requirements include:

- RBI authorization as a payment system operator

- NPCI membership and BBPS certification

- Significant capital requirements (₹1 crore+)

- Dedicated technology and compliance team

Commission Structure

BBPS agent commissions vary by biller category:

| Category | Agent Commission | Avg. Transaction Value |

|---|---|---|

| Electricity | ₹3-10 per transaction | ₹500-2,000 |

| Mobile Postpaid | ₹2-5 per transaction | ₹300-1,000 |

| DTH | ₹2-5 per transaction | ₹200-500 |

| Gas | ₹3-8 per transaction | ₹500-1,500 |

| Insurance Premium | ₹5-15 per transaction | ₹1,000-10,000 |

| Loan EMI | ₹5-20 per transaction | ₹2,000-50,000 |

| Municipal Tax | ₹5-25 per transaction | ₹1,000-50,000 |

An active agent processing 100-200 transactions daily can earn ₹15,000-40,000 monthly.

Technical Integration

Agents typically use one of these interfaces:

- Mobile App: Provided by the AI/COU. Most common for individual agents.

- Web Portal: Browser-based dashboard for agents with higher volumes.

- API Integration: For tech-savvy agents or distributors building their own interface on top of the BBPS API.

- micro-ATM / POS Device: Dedicated hardware for banking correspondent agents.

Getting Started with NxtBanking BBPS

NxtBanking offers a complete BBPS agent platform with multi-biller support, real-time commission tracking, automated settlement, and a white-label agent app. Whether you’re starting as an individual agent or building a distributor network, the platform scales with your business.

Frequently Asked Questions

How much investment is needed to become a BBPS agent?

Starting as an individual agent under a platform like NxtBanking requires ₹5,000-25,000 as working capital. No heavy infrastructure investment is needed — a smartphone with internet is sufficient.

Is BBPS agent business profitable?

Yes. Active agents processing 100-200 transactions daily earn ₹15,000-40,000 monthly. Super agents/distributors with networks of 50+ agents can earn significantly more through override commissions.

What documents are needed to become a BBPS agent?

You need Aadhaar card, PAN card, address proof, bank account details, and a valid business registration (GST or shop establishment license). Requirements vary slightly by Agent Institution.

Can I offer BBPS services through my own app?

Yes. Through NxtBanking’s BBPS API, you can integrate bill payment services into your own branded application. This is ideal for distributors and technology companies building fintech platforms.

Read the complete guide: BBPS API Integration Guide

📚 BBPS Content Hub

About This Topic

Bharat Bill Payment System (BBPS) is NPCI's standardised bill payment network connecting customers with 20,000+ billers across electricity, gas, water, telecom, insurance, and more. NxtBanking's BBPS API enables two-step bill fetch and payment flows with per-transaction BBPS reference numbers, daily MIS reconciliation, dispute management tooling, and a sandbox environment for testing. Integrating BBPS through NxtBanking gives your product access to India's complete utility payment ecosystem under one contract.

Quick Answers

What is BBPS and what does it cover?

BBPS (Bharat Bill Payment System) is NPCI's standardised bill payment network with 20,000+ registered billers spanning electricity, gas, water, telecom, DTH, insurance, education, and municipal services — enabling one-stop bill payment for consumers and businesses alike.

How does BBPS API integration work?

BBPS API integration involves two sequential REST calls: Bill Fetch (retrieve current due amount using the customer's consumer number) and Bill Payment (debit the customer and confirm payment to the biller). Each transaction receives a unique BBPS transaction reference number for traceability.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

Key Terms

- BBPS

- Bharat Bill Payment System — an NPCI-regulated interoperable bill payment network covering 20,000+ billers across electricity, gas, telecom, insurance, and more.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.