BBPS API Charges and Commission Structure

Understanding the BBPS API charges and commission structure is essential for any business planning to enter the bill payment ecosystem in India.

BBPS operates under a regulated framework managed by National Payments Corporation of India, ensuring transparency in pricing and revenue distribution.

For fintech startups, retailers, and distributors, knowing the cost and earning model helps in maximizing profits and planning scalability.

What is BBPS Pricing Model

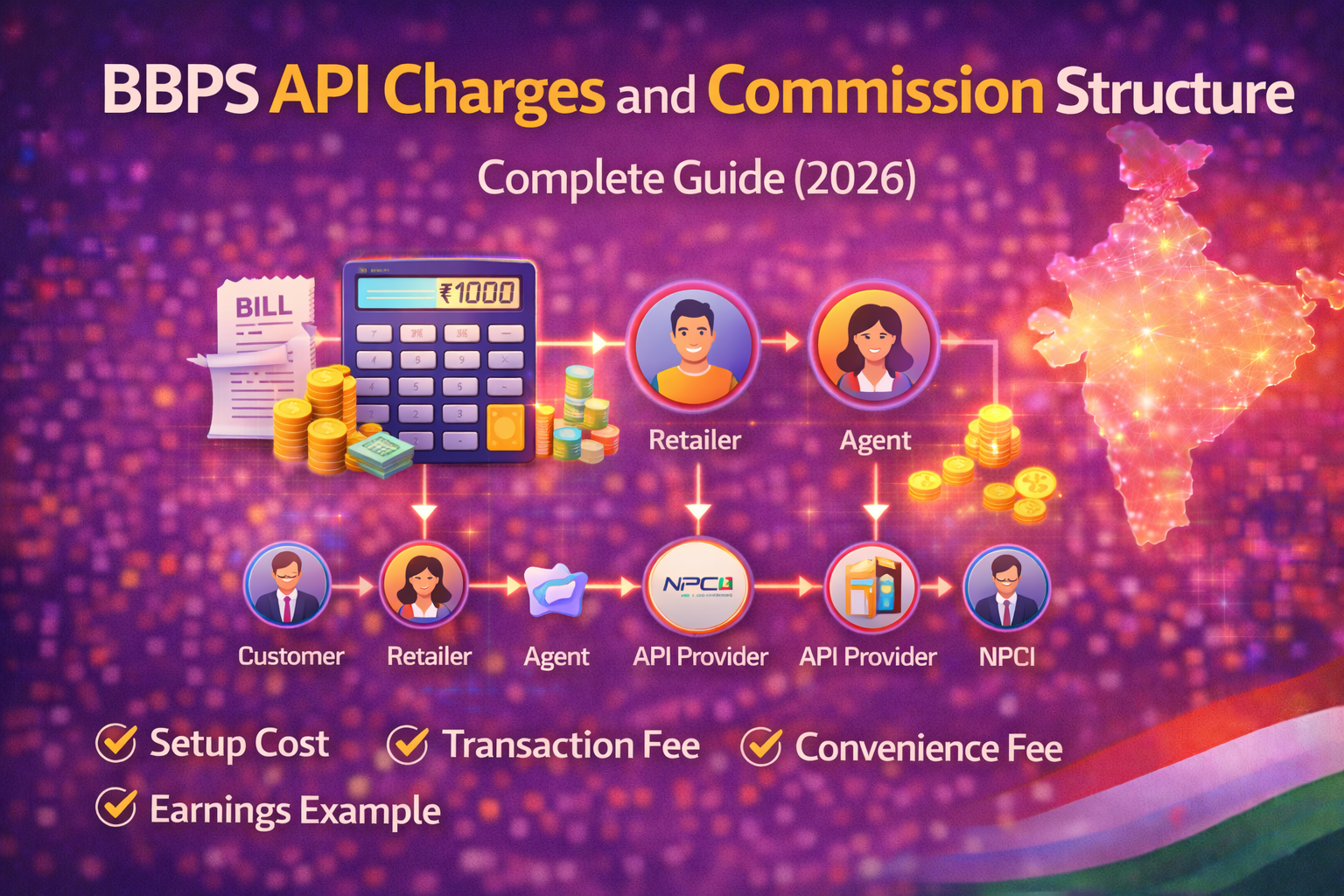

The BBPS API charges and commission structure works on a multi-layer model involving:

- Customer

- Agent / Retailer

- API Provider

- BBPS Operating Unit

- NPCI

Each entity may share a portion of the transaction fee or commission depending on the agreement.

BBPS API Charges Breakdown

Setup Cost

BBPS API providers may charge initial setup fees depending on the business model:

- Basic onboarding: ₹500 – ₹800/year

- Distributor plans: ₹480 – ₹5,555

- White-label solutions: ₹15,000 – ₹25,000

Per Transaction Charges

Most providers charge a small fee per transaction:

- ₹3 – ₹5 per transaction (approx.)

Additionally, NPCI-based charges may apply internally between system participants.

Example:

- Around ₹2–₹3 transaction routing cost in some cases

Convenience Fee (Customer Side)

As per guidelines:

- ₹0–₹5 for bills up to ₹1000

- ₹5–₹15 for mid-range bills

- ₹15–₹25 for higher-value bills

Note:

- Digital payments often have zero convenience fee

- Cash payments may include charges

BBPS Commission Structure

Retailer / Agent Commission

Retailers earn commission on every transaction:

- Typically 1% to 5% per transaction

Distributor Commission

Distributors earn a share from retailer transactions:

- Commission split depends on provider

- Higher volume = higher margins

API Provider Earnings

API providers earn from:

- Transaction charges

- Service fees

- Platform usage

Example of BBPS Earnings

Scenario

- 100 transactions/day

- Avg bill value: ₹1000

- Commission: ₹5 per transaction

Earnings

- Daily: ₹500

- Monthly: ₹15,000

This shows how BBPS API commission structure creates consistent income.

Factors Affecting BBPS Charges and Commission

1. API Provider

Different providers offer different pricing

2. Transaction Volume

Higher volume = better commission

3. Payment Mode

Cash vs digital affects charges

4. Business Type

Retailer, distributor, or fintech platform

5. Biller Category

Different bill types may have different margins

How to Maximize BBPS Profit

To improve earnings:

- Choose high-commission provider

- Increase transaction volume

- Offer multiple services

- Focus on high-demand areas

- Provide fast and reliable service

https://nxtbanking.com/bbps-api

https://nxtbanking.com/dmt-api

https://nxtbanking.com/aeps-api-provider

Why BBPS is Profitable

The BBPS API charges and commission structure is designed to:

- Ensure fair distribution of revenue

- Encourage agent participation

- Promote digital payments

Businesses benefit from:

- Recurring income

- Low operational cost

- Scalable model

FAQs

What are BBPS API charges

BBPS API charges include setup fees, transaction fees, and optional service charges depending on the provider.

How much commission can I earn in BBPS

Typically 1% to 5% per transaction depending on volume and provider.

Is BBPS API profitable

Yes, it offers consistent earnings with low investment and high demand.

Who decides BBPS charges

Charges are regulated by NPCI and implemented by BBPS providers.

Conclusion

The BBPS API charges and commission structure provides a balanced ecosystem for all participants.

With low setup costs, recurring commissions, and increasing demand for digital payments, BBPS remains one of the most profitable fintech opportunities in 2026.

Businesses that understand and optimize this structure can build a strong and scalable revenue model.

About This Topic

Bharat Bill Payment System (BBPS) is NPCI's standardised bill payment network connecting customers with 20,000+ billers across electricity, gas, water, telecom, insurance, and more. NxtBanking's BBPS API enables two-step bill fetch and payment flows with per-transaction BBPS reference numbers, daily MIS reconciliation, dispute management tooling, and a sandbox environment for testing. Integrating BBPS through NxtBanking gives your product access to India's complete utility payment ecosystem under one contract.

Quick Answers

What is BBPS and what does it cover?

BBPS (Bharat Bill Payment System) is NPCI's standardised bill payment network with 20,000+ registered billers spanning electricity, gas, water, telecom, DTH, insurance, education, and municipal services — enabling one-stop bill payment for consumers and businesses alike.

How does BBPS API integration work?

BBPS API integration involves two sequential REST calls: Bill Fetch (retrieve current due amount using the customer's consumer number) and Bill Payment (debit the customer and confirm payment to the biller). Each transaction receives a unique BBPS transaction reference number for traceability.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

Key Terms

- BBPS

- Bharat Bill Payment System — an NPCI-regulated interoperable bill payment network covering 20,000+ billers across electricity, gas, telecom, insurance, and more.

- API

- Application Programming Interface — a structured software interface that lets applications communicate with each other over the internet using defined endpoints, authentication, and data formats.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.