How to Choose an AEPS API Provider in India: 7 Criteria

Selecting an AEPS API provider impacts every retailer in your network. Shortlist vendors with proven BC deployments and clear escalation paths. NxtBanking’s AEPS API India page outlines our stack.

Checklist

- Uptime and incident history

- Bank and sponsor coverage

- Agent onboarding and KYC tooling

- Compliance documentation

- 24/7 support for field issues

- Transparent commercials

- Product roadmap (MATM, DMT bundle)

Related: Best payout API · BBPS API · AEPS API · Mobile recharge API · Request demo

How to Choose the Best AEPS API Provider in India

Choosing the right AEPS API provider is one of the most critical decisions for your fintech or banking business. A poor choice can result in high failure rates, slow settlements, and unhappy customers. Here’s a comprehensive guide to help you make the right decision.

1. Check NPCI Authorization

Only work with AEPS API providers who are authorized by NPCI (National Payments Corporation of India) or are connected through an NPCI-licensed Technical Service Provider (TSP). This ensures regulatory compliance and transaction protection.

2. Evaluate Transaction Success Rate

A good AEPS API provider should maintain a transaction success rate of 97% or above. Ask for historical performance data. NxtBanking maintains a 98.5%+ success rate across all AEPS transactions.

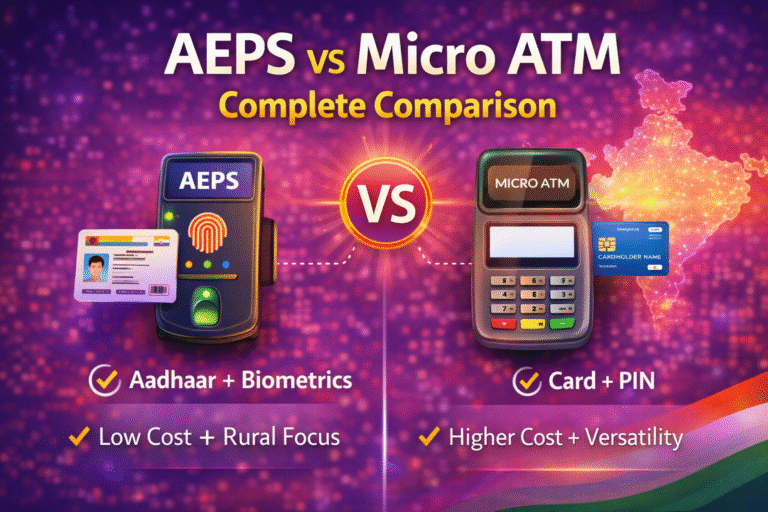

3. Check Multi-Bank Support

AEPS relies on bank connectivity. The more banks your provider supports, the higher your success rate. NxtBanking supports AEPS across all major public sector and private banks, including SBI, PNB, Bank of Baroda, Canara Bank, HDFC, ICICI, and more.

4. Settlement Speed and Reliability

T+0 (same-day) settlement is ideal for AEPS businesses. Check if your provider offers instant settlement or if there are delays. Delayed settlements can create cash flow issues for CSP operators and agents.

5. API Documentation Quality

A well-documented API reduces integration time from weeks to days. Look for providers that offer:

- Complete API reference with request/response examples

- Postman collections for quick testing

- Sandbox environment for development

- Code samples in multiple languages (PHP, Python, Node.js, Java)

6. Pricing and Margin Structure

Transparent pricing is a sign of a trustworthy provider. Compare per-transaction costs, monthly fees, and reseller margin structures. Avoid providers with hidden charges or opaque billing.

7. Technical Support Availability

AEPS transactions happen 24/7, including weekends and holidays. Your API provider must offer round-the-clock technical support. NxtBanking provides dedicated account managers and 24/7 helpdesk for all AEPS clients.

AEPS API Provider Comparison Checklist

- ☑ NPCI authorized or connected through licensed TSP

- ☑ 97%+ transaction success rate

- ☑ 100+ bank support

- ☑ T+0 or T+1 settlement

- ☑ Real-time dashboard and reports

- ☑ White-label capability for branded apps

- ☑ 24/7 technical support

- ☑ Competitive commission structure

About This Topic

AEPS (Aadhaar Enabled Payment System) is India's biometric banking service that gives rural and unbanked populations access to cash withdrawal, balance enquiry, and mini statement through Business Correspondent outlets. Built on UIDAI's Aadhaar authentication infrastructure and operated by NPCI, AEPS removes the dependency on bank cards and PINs. NxtBanking's AEPS API provides fintechs and BC networks with a reliable, multi-bank connected integration covering all AEPS transaction types with 99.9% uptime, real-time webhooks, and full NPCI compliance.

Quick Answers

What is AEPS and how does it work?

AEPS (Aadhaar Enabled Payment System) is an NPCI-operated banking service that authenticates customers using their Aadhaar number and biometric fingerprint, allowing cash withdrawal, balance enquiry, and mini statement at Business Correspondent points without a debit card or PIN.

Who can use AEPS?

Any Indian resident with an Aadhaar-linked bank account can use AEPS at a registered BC or Micro-ATM outlet. It is specifically designed for rural and unbanked populations who lack access to physical bank branches or ATMs.

Is NxtBanking RBI-compliant for payment APIs?

Yes. NxtBanking operates through RBI-licensed partner banks for all payment services (IMPS, NEFT, RTGS, UPI) and is NPCI-certified for BBPS, AEPS, and UPI flows. All APIs follow RBI's Master Directions on payment aggregators, KYC, and PMLA obligations. We maintain audit logs, data localisation, and consent frameworks compliant with the DPDP Act 2023.

How does NxtBanking handle API downtime and failover?

NxtBanking uses a connected-banking architecture that links a single API credential to multiple RBI-licensed partner banks. When one bank's rails experience degradation or maintenance, the API automatically routes to the next available bank — with no code change required on the client side. This multi-bank failover is what delivers 99%+ transaction success rates and 99.9% API uptime SLA for enterprise clients.

What does it cost to integrate NxtBanking APIs?

NxtBanking offers pay-as-you-go pricing with no setup fees and no minimum commitment for most APIs. Typical pricing: IMPS/UPI payout ₹3–₹8 per transaction, NEFT ₹1–₹3, BBPS bill payment ₹0.50–₹3, AEPS cash withdrawal ₹2–₹5. Enterprise clients on committed volumes negotiate flat-rate pricing. Sandbox access is free and unlimited. Contact sales for a custom quote based on your expected transaction volume.

Key Terms

- AEPS

- Aadhaar Enabled Payment System — a bank-agnostic cash withdrawal and balance enquiry service authenticated via Aadhaar biometrics, operated under NPCI.

- API

- Application Programming Interface — a structured software interface that lets applications communicate with each other over the internet using defined endpoints, authentication, and data formats.

NxtBanking is India's AI-powered fintech API platform trusted by hundreds of fintechs, BC networks, NBFCs, and enterprise companies. Our unified API marketplace covers payout (IMPS, NEFT, RTGS, UPI), BBPS bill payment with 20,000+ billers, AEPS biometric banking, KYC and identity verification (Aadhaar, PAN, Bank, Driving Licence, Voter ID, RC), UPI collection and QR codes, domestic money transfer (DMT), mobile and DTH recharge, Micro-ATM, and travel APIs — all under one master agreement, one set of credentials, and one consolidated monthly invoice.

Every NxtBanking API is backed by a 99.9% uptime SLA, real-time webhook delivery, a full-featured sandbox environment with simulated error scenarios, comprehensive API documentation with Postman collections and code samples in multiple languages, and dedicated technical onboarding support. Production go-live for most APIs is achievable within 7–15 business days after KYC and compliance review. For enterprise clients requiring custom SLAs, dedicated infrastructure, or white-label platform builds, NxtBanking offers tailored commercial terms with no minimum volume commitment at the pilot stage.