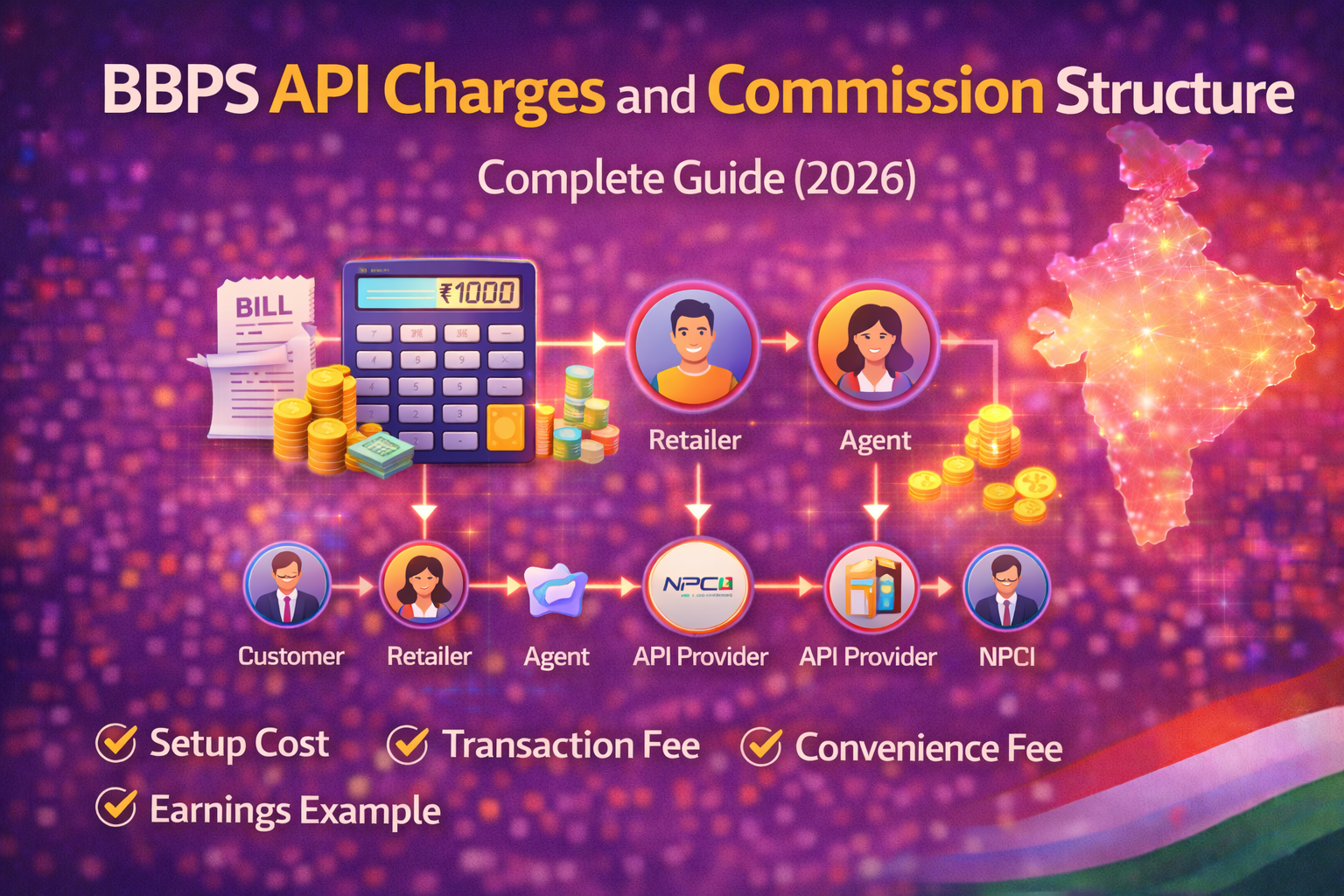

BBPS API Charges and Commission Structure

Understanding the BBPS API charges and commission structure is essential for any business planning to enter the bill payment ecosystem in India.

BBPS operates under a regulated framework managed by National Payments Corporation of India, ensuring transparency in pricing and revenue distribution.

For fintech startups, retailers, and distributors, knowing the cost and earning model helps in maximizing profits and planning scalability.

What is BBPS Pricing Model

The BBPS API charges and commission structure works on a multi-layer model involving:

- Customer

- Agent / Retailer

- API Provider

- BBPS Operating Unit

- NPCI

Each entity may share a portion of the transaction fee or commission depending on the agreement.

BBPS API Charges Breakdown

Setup Cost

BBPS API providers may charge initial setup fees depending on the business model:

- Basic onboarding: ₹500 – ₹800/year

- Distributor plans: ₹480 – ₹5,555

- White-label solutions: ₹15,000 – ₹25,000

Per Transaction Charges

Most providers charge a small fee per transaction:

- ₹3 – ₹5 per transaction (approx.)

Additionally, NPCI-based charges may apply internally between system participants.

Example:

- Around ₹2–₹3 transaction routing cost in some cases

Convenience Fee (Customer Side)

As per guidelines:

- ₹0–₹5 for bills up to ₹1000

- ₹5–₹15 for mid-range bills

- ₹15–₹25 for higher-value bills

Note:

- Digital payments often have zero convenience fee

- Cash payments may include charges

BBPS Commission Structure

Retailer / Agent Commission

Retailers earn commission on every transaction:

- Typically 1% to 5% per transaction

Distributor Commission

Distributors earn a share from retailer transactions:

- Commission split depends on provider

- Higher volume = higher margins

API Provider Earnings

API providers earn from:

- Transaction charges

- Service fees

- Platform usage

Example of BBPS Earnings

Scenario

- 100 transactions/day

- Avg bill value: ₹1000

- Commission: ₹5 per transaction

Earnings

- Daily: ₹500

- Monthly: ₹15,000

This shows how BBPS API commission structure creates consistent income.

Factors Affecting BBPS Charges and Commission

1. API Provider

Different providers offer different pricing

2. Transaction Volume

Higher volume = better commission

3. Payment Mode

Cash vs digital affects charges

4. Business Type

Retailer, distributor, or fintech platform

5. Biller Category

Different bill types may have different margins

How to Maximize BBPS Profit

To improve earnings:

- Choose high-commission provider

- Increase transaction volume

- Offer multiple services

- Focus on high-demand areas

- Provide fast and reliable service

https://nxtbanking.com/bbps-api

https://nxtbanking.com/dmt-api

https://nxtbanking.com/aeps-api-provider

Why BBPS is Profitable

The BBPS API charges and commission structure is designed to:

- Ensure fair distribution of revenue

- Encourage agent participation

- Promote digital payments

Businesses benefit from:

- Recurring income

- Low operational cost

- Scalable model

FAQs

What are BBPS API charges

BBPS API charges include setup fees, transaction fees, and optional service charges depending on the provider.

How much commission can I earn in BBPS

Typically 1% to 5% per transaction depending on volume and provider.

Is BBPS API profitable

Yes, it offers consistent earnings with low investment and high demand.

Who decides BBPS charges

Charges are regulated by NPCI and implemented by BBPS providers.

Conclusion

The BBPS API charges and commission structure provides a balanced ecosystem for all participants.

With low setup costs, recurring commissions, and increasing demand for digital payments, BBPS remains one of the most profitable fintech opportunities in 2026.

Businesses that understand and optimize this structure can build a strong and scalable revenue model.